For many, it appeared as though the advent of 5G was the death knell for value-added services (VAS). Over The Top (OTT) providers and third-party vendors are cannibalizing revenue that operators previously generated from non-essential services, like ringtones, balance check, resource sharing, etc.

But despite the challenges that the telecommunications industry is facing, the market for value-added services is still growing, and operators have new opportunities to increase their revenue – provided they pivot strategically and act quickly.

Vodafone’s success in delivering tailored, innovative VAS to regions with limited access to banking is a prime example of the modern-day potential for value-added services. And while a focus on 5G pushes operators to alienate certain audiences – e.g., those with feature phones and low connectivity – these subscribers may be most receptive to VAS.

In this article, we’ll explore the skepticism surrounding VAS in telecom and the potential for operators to increase their revenue with innovative services.

Why is VAS surrounded by skepticism?

Before we start explaining VAS’s importance and potential, let’s look at why there is skepticism about the relevance of VAS in the first place.

1. Growing competition from OTT (over the top) providers

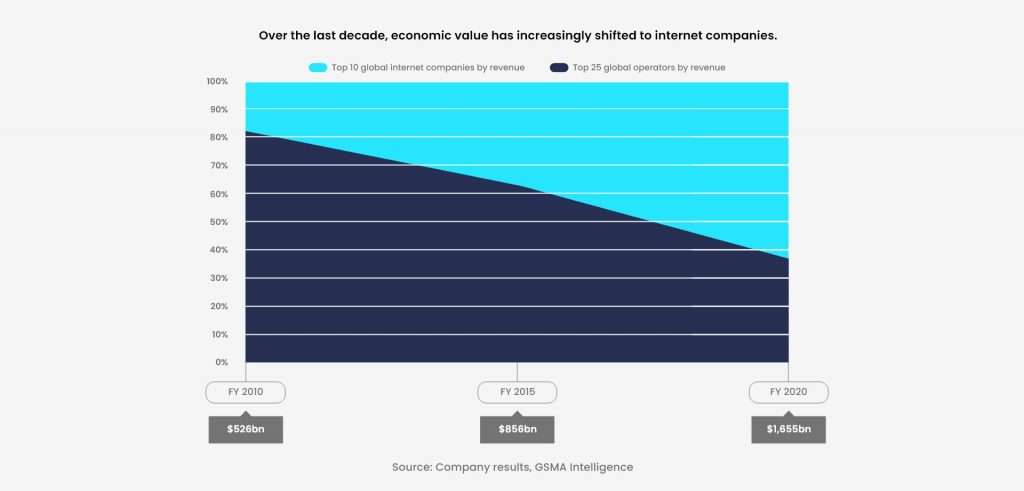

OTT services are media services directly provided to consumers through the internet. Some examples of OTT providers are Netflix, Hulu, and WhatsApp. These OTT providers have gradually taken over markets that were previously dominated by telecom operators.

A report by McKinsey & Company revealed that the share of relevant revenue from messaging, fixed voice, and mobile voice provided by OTT players went from 9, 11, and 2 in 2011 to 40, 25, and 7 percent in 2018, respectively, in an all-IP environment. This is especially true for services originally provided through VAS.

Why subscribe to a radio service when you can hear a podcast for free on the internet or on an app?

These numbers starkly contrast the dynamic that existed between telcos and OTT service providers two decades ago. One reason for this shift is that, traditionally, VAS did not benefit OTT or third-party vendors as much as telcos themselves.

When OTTs or third-party vendors ventured into value-added services, the offerings were not accredited to them, contextual customer data (e.g., demographic data) was not shared with them, and they were under strict regulations.

Meanwhile, the telco merely facilitated them while benefiting from the generated revenue. So naturally, when 4G and 5G penetrated the market, third parties decided to cut out the middleman and developed feature-rich apps that supplanted VAS.

2. Traditional expectations of VAS

Unfortunately, while the market changed with 4G and 5G, the expectations from VAS remained the same. VAS was expected to produce the same ROI as when feature phones were popular and short code dial-ups were the primary method to access media services. This is no longer the case, but the industry is struggling to innovate.

For example, a dated value-added service allowed users to change their ringtone via a code. But dialing a code and sitting through a lengthy, automated call just to change your ringtone is inefficient now. There are quicker, more convenient alternatives, so operators need to explore services that deliver value to today’s consumers.

3. Operators risk alienating communities

According to Telecoms.com’s 2021 Annual Industry Survey, all telecom operators plan to invest in new technologies to increase their competitive edge. The survey also revealed a strong alignment between priority investments, with the top 3 investment areas being:

- 5G initial deployment

- Digital transformation

- 5G densification.

However, this focus on new technologies, and 5G in particular, pushes operators to prioritize specific customer bases – at the cost of alienating others. Thus, 5G adoption involves further disassociation from traditional VAS as operators continue to prioritize smartphone users.

In developing countries, this change marginalizes a major customer base that relies on feature phones or suffers from poor connectivity.

VAS isn’t dead, though. And here’s why:

A simple market overview reveals that VAS is still growing. The global mobile value-added services market was valued at US$630.52 billion in 2020, with an estimated CAGR of 10.1% from 2021 to 2031. These numbers suggest that VAS is still relevant to both telecom operators and their customers – but why is that?

Let’s find out.

1. The opportunity to innovate

While the number of smartphone users increases and 5G adoption grows, telcos face revenue cannibalization from OTT service providers and global internet companies to their core services (like calling and messaging features). It is not enough for telcos to compete on these core services alone – operators need to think ahead and innovate with VAS to complement their core offerings.

OTT players add value to their core services and have special services for specific customers (e.g., WhatsApp Business) to help distinguish themselves. Similarly, telecom operators can stand out by incorporating innovation into their value-added services, in addition to delivering cutting-edge core services.

2. Customer bases in the developing world

While the global trend indicates more smartphone adoption, the developing world’s situation is skewed. Smartphone penetration in these regions is relatively much lower, especially in highly populated developing countries, like India (at 35.4%), Nigeria (having 19.7%), and Pakistan (at 20.9%).

A key driver here is the economic constraints and low disposable income, restricting a large part of the population to feature phones. These users still demand content-oriented, value-added services such as radio, SMS updates on sports matches, etc. Additionally, there is demand for niche value-added services amongst users that aren’t literate or have disabilities. For these subscribers, utilities like voice-activated calls are a niche VAS can fulfill.

The way forward – 6 ways to add value in VAS

So, VAS can be beneficial, but how do you add value to your VAS to make it competitive, and relevant to your subscribers?

1. Venture into utility VAS

As long as voice calls and SMS remain popular channels amongst subscribers, associated VAS will still have demand, even in the developed world. Here are four ways operators can deliver additional utility services to subscribers:

- Beep call & beep message: Allows telco users to send a beep call or a beep message to notify the receiver that the user is trying to reach them.

- Additional Number: Let users get an additional number with their primary SIM, so they don’t have to carry two phones.

- Data saver service: This value-added service lets users store a specific amount of data by subscribing to a data saver service. This data is only consumed when they dial a short code, allowing them to retain data for urgent tasks.

- Voice dial: Let subscribers use their voice to dial saved numbers from their contact list.

2. Personalize your VAS

Personalizing your services is an effective way to improve user experience, by enhancing your subscribers’ convenience, increasing the relevancy of your content, delivering targeted promotions, etc.

The key considerations here are:

- Building a customer profile that you can use to refine your features, content, and interface.

- Geography – targeting region-specific markets.

- And specialization – develop features that cater to a specific market.

These considerations can help operators tailor their offerings and deliver better experiences. For example, telcos can segment customers on their spending habits and sort them into higher income brackets. These segments are better suited for targeting with big-ticket offers.

Some brands, like Vodafone, use geography to tailor their offering. For example, Vodafone believes its cash app, M-PESA (Africa) is successful because it targets a market where people have limited access to banking, and limited convenient and secure services for transactions. Another example is WeChat, which was successful due to China’s ban on social media outlets.

3. Synergy among your services

Operators can unlock more potential for value-added services by considering how they may enhance the user experience in other areas. For example, some telcos that offer cash apps also allow users to purchase mobile games using the application. A deeper understanding of customer needs helps operators discover and refine new value-added services.

4. Promotion-based payment systems

When developing apps for delivering value-added services, telcos can generate revenue by switching to a promotion-based system. Here, instead of charging subscribers for value-added services, operators can deliver the services for free and generate revenue from advertisements.

This advertisement model is popular in digital advertising – ads from search engines, videos, and banners are the most popular revenue-generating streams. So, it’s an interesting potential revenue stream for operators to consider, as the model has proven successful in the digital medium.

Lastly, operators can potentially increase their revenue further by offering premium services for a subscription, upselling users from your free services.

5. Content-rich and innovative VAS

For smartphone users, operators can penetrate the massive OTT market (projected to reach over a trillion dollars by 2027) by developing relevant media services. Global operators have penetrated this market by developing apps in-house (e.g., My Verizon app), or partnering with OTT service providers. For example, Vodafone’s Vodafone TV has secured partnership contracts with Netflix and Amazon Prime.

For this strategy to be successful, your offering needs to be in response to consumer demand. The content needs to be tailored to meet this demand – for example, consider live updates during a global sports event. Moreover, operators can reduce friction to make the services more user-friendly, by reducing the clicks required to access the services, and making it easy to scroll and subscribe.

6. B2B VAS

The growth of the 5G enterprise market has created new opportunities for telcos to aid enterprises in digital transformation, cybersecurity, and cloud infrastructures. For example, telcos can leverage their expertise to build cloud on-ramps/cloud connect services for enterprises – i.e., private pathways that connect an enterprise’s IT infrastructure to a public cloud.

A report by McKinsey discussed how operators have more to gain by prioritizing transversal products, such as cybersecurity, IoT, and cloud services for regional SMB segments. Otherwise, telcos are at risk of failing due to competition from existing major players. For example, Verizon acquired Terremark to establish cloud services, but the venture failed because they were unable to scale and compete with tech giants like Microsoft, Amazon, and Google.

Another opportunity for telcos resides in 5G deployment amongst enterprises, which invites cybersecurity concerns. The biggest concern for organizations looking to adopt 5G is the risks associated with data mismanagement and updating data security management programs. These risks exist due to the sheer volume and diversity of data.

Thus, operators are in a unique position to provide enterprises with value-added services to mitigate cybersecurity risks.

The bottom line: Innovation paves the way forward

Telecom operators are navigating a highly competitive landscape, where they’re not only threatened by competing operators, but also third parties like OTT providers. And while some argue that VAS is dead, we’ve found that, on the contrary, innovative VAS is key to unlocking new revenue streams and consolidating subscriber bases.

Thus, while it is clear that VAS is facing challenges, to say it is dead is simply incorrect. Operators that prioritize customer experience, and deliver value-added services tailored to their subscribers’ needs, may discover new opportunities for growing their revenue.